|

|

|

|

|

Best Pension Annuity is a trading style of Platinum Financial Consulting LTD

AUTHORISED & REGULATED BY THE FINANCIAL CONDUCT AUTHORITY |

|

|

|

We do all the work for you - We calculate your entitlement - We deal with your pension providers - We keep you updated |

This page is full of information on Flexible Drawdown and eligibility rules.

By reading this page you will gain a good knowledge of flexible drawdown and the conditions you will need to satisfy if you want to take advantage of it. There are also a number of case studies which will help you understand how flexible drawdown may work in various scenarios.

We also provide links to our flexible drawdown calculator and give you the ability to apply for a bespoke quote and our help in using your pension funds in line with the eligibility rules. |

|

An in-depth guide to flexible drawdown |

|

One of the most compelling reasons people choose income drawdown is the fact that any money that isn’t taken as a tax free lump sum and / or income remains under their control. The pension fund is still owned by the customer, it is not given away to an annuity company. Of equal importance to some customers is the ability to take out the majority, if not all, of the fund in the early years of their retirement. There are many customers we deal with who, if they could, would take their entire fund as a lump sum, or a series of lump sums over a few years. However until recently this has not been possible. The UK Government need people to save for their retirement, so that when they eventually stop working they will have enough money of their own to provide an income in retirement. To encourage people to save for retirement very attractive tax incentives have been offered to pension savers, however these tax breaks do come at a price – mainly by placing some restrictions on how the money is taken out of the pension fund.

Imagine how much harder things would be for the Government if somebody who had a large pension fund, was able to take it all when they retired. They could choose to blow it all on extravagant holidays, fast cars and other luxuries. However if they spent it all in the first year, they would have no income for the remaining years of their retirement and would be dependent upon state benefits and the tax payer. Therefore the Government’s primary aim with pension planning is to make the pension last for a person’s entire lifetime.

With respect to income drawdown, the way of controlling how much income is taken from a pension assesses the average life span of people of various ages. This allows them to calculate a percentage, which is then used to calculate how much income can be taken from the fund. The percentage used is based upon your life expectancy, the aim being that (assuming no growth or loss in your fund value other than the income you are taking) the amount taken should be enough to sustain an income for your life. However this is not guaranteed. In very simple terms, if your fund was worth £100,000 and your GAD rate was 5% then you would be able to take £5,000 income from the fund (100% GAD). Currently you can take a maximum of 120% of the GAD limit, using this example £6,000.

All of the above applies to customers who don’t have other retirement income, or retirement income of less than £20,000 from other pension sources.

In April 2010 the Government changed the income drawdown rules, to recognise that for some customers it may be in their best interests to take all of their money out of their pension fund. These people would be able to use their pension fund as they wished, but their circumstances should prevent them becoming a burden on the state. The government would allow a customer to use their pension fund as they wished, as long as the customer had guaranteed pension income of £20,000 per annum from other pension sources. They therefore introduced the concept Flexible Drawdown for people who meet this criterion.

|

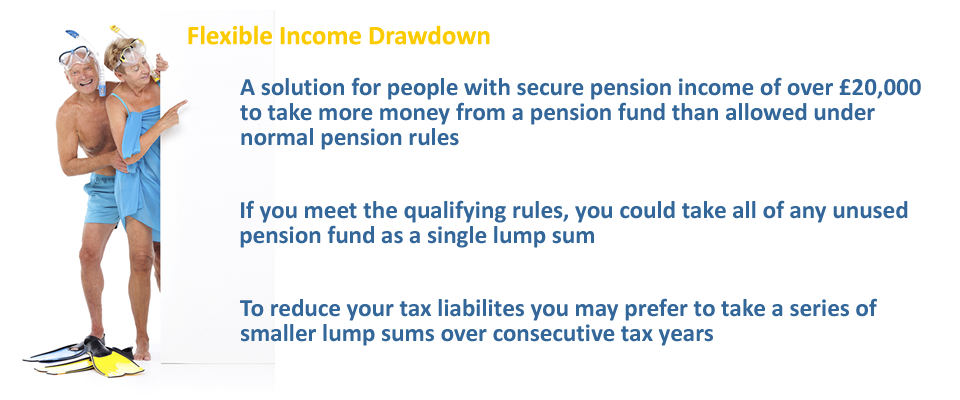

What is Flexible Drawdown?

|

Flexible Drawdown is available to customers who meet the Governments ‘Minimum Income Requirement’ (MIR) – which we will discuss soon. If you meet the MIR then the GAD limits do not apply to you and you can take as much money out of your pension plan as you want. It will be subject to income tax at your marginal level. This means that a customer can use the money as they see fit even if it means paying a higher rate of tax.

Any pension money that is still under your control, after you meet the qualifying criteria, can be used for flexible drawdown. The government have set the rules in a way that the MIR must be made up from regular retirement income - generally from products and sources that are not under you direct control and are guaranteed to be paid to you for your entire life.

If you have not yet touched the pension fund (in other words your fund is uncrystalised) then standard retirement benefits are still available to you – perhaps the most important being the ability to take 25% of the fund as a tax free lump sum. Assuming you qualify for flexible drawdown you can take 25% of an uncrystalised fund tax free. The remaining 75% can be taken as one 75% taxable lump sum, or a series of equal taxable lump sums over a few years. The latter approach may help a customer realise their entire fund at lower tax rates.

Even if you meet the MIR requirements, Flexible Drawdown may not be suitable for you – this is something you may need to consider. To help you we have included a few case studies below to help identify when flexible drawdown may be suitable.

|

The Minimum Income Requirement (MIR)

|

We have already discussed the fact that the current level for the MIR is £20,000 per annum. This money must come from recognised pension sources, which are guaranteed for life. Products that can be used to contribute towards the MIR are :

|

|

State Pensions (including SERPS and the Second State Pension S2P) |

| Pension Annuities |

| Company Pensions (final salary and defined benefit) |

| Scheme Pensions (similar to company pensions) |

| Dependants’ Annuities, Company and Scheme Pensions |

|

As you will see, all of the pensions above will be guaranteed for life and you can have no direct control over them. Products such as Income Drawdown and Temporary annuities do not count towards the MIR.

If you have a with-profits or unit linked annuity, these can count towards the MIR, but only at the minimum guaranteed level of the product.

|

Using a dependant’s annuity to calculate MIR

|

If you have unused pension funds and want to use flexible drawdown, you can use annuities, company and scheme pensions that belong to your partner to count towards your MIR calculation. However you can only use those pensions and annuities if you are entitled to receive a dependant’s benefit from those pensions and annuities, and then only to the level of benefit you would be entitled to. The HMRC website is not very clear on the use of dependants’ pensions in calculating MIR and our assessments in this section are based upon how providers seem to be addressing this issue. The approach, in our view, is also a common sense approach when viewed in the light of other products HMRC use to address the MIR. HMRC Technical

In simple terms if your partner has a pension and in the event of their death you would receive all or a portion of it for the remainder of your life, then you could build your entitlement from their pension into your MIR calculation. For example, if your partner has an annuity paying them £10,000 per annum and in the event of their death you would continue to receive half of it until your death, then you could claim £5,000 to count towards the MIR calculation.

|

|

| |

They each have an unused pension fund worth £20,000. So far they have not taken any benefits from these funds.

Question : Rather than take another annuity they would prefer to have all of the unused pension funds as a lump sum. Can they take it all as a lump sum of £40,000. If not what is the maximum they could take as a lump sum ?

Answer : To take it all as a lump sum they must both qualify for flexible drawdown. We therefore need to check if they can both meet the MIR of £20,000 p.a.

Barbara has £15,000 p.a. from her annuity. She would also receive half of Tom’s annuity should he die. This would be £7,500 p.a. We add this to her own annuity income giving her an annual income, for MIR purposes, of £22,500. As this is in excess of the MIR Barbara can take all of the £20,000 unused pension fund as a lump sum. The first 25% (£5,000) would be paid tax free but the remaining £15,000 would be eligible to income tax at Barbara’s marginal rate.

Although Tom’s annuity and pensions are very similar to Barbara’s, he will not receive any of Barbara’s annuity should she die. Therefore his maximum annual income, for MIR purposes is £15,000. This means he does not qualify for flexible drawdown and therefore can only take his pension fund in the conventional manner. He can take a maximum tax free lump sum of £5,000, but the remaining £15,000 must be used to buy an annuity, income drawdown or other retirement product.

Therefore the maximum lump sum they can take from their combined unused pension funds is £25,000. (Barbara £20,000 + Tom £5,000). |

|

|

|

Other Flexible Drawdown Conditions

|

While the key condition is the Minimum Income Requirement (discussed above) there are other conditions you will need to satisfy in order to qualify for flexible drawdown.

The £20,000 MIR must be achieved / achievable in the tax year in which you wish to enter flexible drawdown.

You must have ceased to be a member of any “defined benefit” scheme of which you were a member. Even if you are no longer making contributions or are not accruing benefits you will still be classified as a member if the benefits within the scheme are linked to your current salary.

You cannot make any contributions to any money purchase arrangement (or have contributions made on your behalf by any third party) in the tax year in which you wish to go into flexible drawdown. For example, if you make a single contribution to a money purchase scheme in May, you will be ineligible for flexible drawdown for the remainder of that tax year. Assuming no contributions are made in the following tax year, you would be eligible for Flexible Drawdown from the following April.

You can re-start to make pension contributions, if you wish, from the tax year after the tax year you entered flexible drawdown.

|

|

| |

The FSAVC is worth £30,000. He did not use this fund at retirement, deciding to use it when he was older.

He has considered an annuity. After tax free cash of £7,500, the annuity will provide him with £1,500 per annum.

Question : James doesn’t really need the additional income and would rather use the £22,500 to buy a touring camper van for himself and his wife. Can he do this ?

Answer : As James has an annual income from his teachers’ pension (which is guaranteed for life) of £25,000 he qualifies for flexible drawdown. This means he can take any other unused pension funds as a lump sum. He decides to use flexible drawdown to take tax free cash of £7,500 from the fund and the remaining £22,500 as a lump sum to help fund the purchase of the camper van.

|

|

|

|

Tax Efficiency |

While the idea of taking all of your pension fund as a lump sum may sound attractive, if your fund is particularly large and / or your income is also in (or close to) the higher tax thresholds, then you could be paying considerable amounts of tax if you take all of your fund in one go.

This would be particularly frustrating if you have no specific purpose for the money, but would prefer it as a lump sum rather than being forced to buy an income. However it should be remembered that after the standard 25% tax free lump sum entitlement, all further lump sums taken from flexible drawdown are treated as earned income for the purposes of tax.

Our selected provider will enable you to enter income drawdown and take a series of smaller lump sums over a number of consecutive tax years. This could enable a customer to keep the income (lump sums) taken from flexible drawdown below a higher tax threshold. As an example a customer who qualifies for flexible drawdown with £40,000 in a pension fund, would move into a higher rate tax bracket if their income increases by more than £12,000 during the tax year. If they took all of the fund in one go, this would undoubtedly be the case. However if they chose to take it over three consecutive tax years they could avoid paying the higher rate of tax.

In the first year they decide to take £20,000. This being made up of their 25% tax free cash of £10,000 and one third of the remaining £30,000, another £10,000. This £10,000 although subject to tax keeps the client below the higher rate tax band. The customer then takes a further £10,000 for the following two tax years which then exhausts their fund.

|

|

| |

Question : Julia would like to take more than 25% as a lump sum from her pension to buy a holiday home abroad. As this is her only pension fund she doesn’t currently have any pension income. How can she take more than 25% as a lump sum?

Answer : Fortunately for Julia her fund is sufficiently large enough to allow her to manage it to her advantage. The first step is to create an income that meets the Minimum Income Requirement (MIR). If she were to use £375,000 of her fund to buy an annuity, this would give her an annual income of just over £20,000 which would be sufficient to meet the MIR. Fortunately Julia would be happy with this level of income !!

We therefore take half of Julia’s pension fund (£500,000) and use it to buy an annuity. She will get £125,000 as a tax free lump sum, and the remaining £375,000 buys the annuity. The unused £500,000 is placed in a separate pension fund.

Julia now meets the MIR and the unused pension fund is eligible for flexible drawdown.

She places the remaining £500,000 into Flexible Drawdown. Again she takes her tax free cash entitlement of £125,000.

While she could take the remaining £375,000 as a single lump sum, she decided not to take it all as one lump sum to avoid paying the highest rate of tax on the majority of it (45% in 2013/14). She therefore decides to take it over 5 years. She will therefore receive £75,000 for 5 years which will be subject to income tax.

This will give her a lump sum of £325,000 in her first year, which is sufficient to buy the holiday home.

This is made up of £125,000 tax free cash when buying the annuity, a further £125,000 tax free cash when she went into flexible drawdown, and £75,000 which is her first year’s flexible drawdown payment. This means that in the first year she has released a lump sum equating to 32.5% of the fund value. At the end of 5 years, she will have released 62.5% of her original fund via a series of lump sums.

| |

|

|

Investment Risk |

While the concept of taking flexible drawdown over a period of consecutive tax years will appeal to many high rate tax payers, they may be concerned about the impact that future investment performance could have on their fund while it remains within the flexible drawdown contract.

Our selected product will completely remove investment risk from your flexible drawdown fund. While you will not gain if markets increase, you will not lose any of your fund should markets crash and you have not yet completed taking the series of lump sums from the contract.

Before your contract starts you will receive a quote based on your fund value, which will include all the costs for the product deducted at outset. This will leave a figure which will represent your flexible drawdown entitlement. This figure will be paid to you in its entirety during the term of your flexible drawdown contract. You can also take it as a single lump sum if you wish.

If for example, after taking tax free cash and deducting our charges the quote shows a flexible drawdown pot of £100,000 and you opt to take it over 5 years, then you will receive £20,000 per annum (before tax) from the fund each year, irrespective of what happens to investment returns. If the amount transferred by your existing product provider was different to the amount quoted then the amount payable from your flexible drawdown contract would increase or decrease accordingly.

|

Useful Links |

| |

Trivial Commutation - Terms and Conditions |

These terms and conditions run in tandem with our general business terms and conditions contained on this website.

These additional Flexible Drawdown conditions only apply when a customer has selected to use our Flexible Drawdown service.

Where there is a conflict between our general terms and conditions and these terms and conditions for flexible drawdown, the flexible drawdown terms and conditions shall be given precedent if the customer has applied for the flexible drawdown service.

The flexible drawdown terms and conditions do not apply to any other transactions or services offered by Best Pension Annuity.

When a customer selects to use our flexible drawdown service, engaging us by our web forms, telephone, email or post, these terms and conditions are immediately binding and the service shall have been deemed to commence.

Platinum Financial Consulting (Platinum) trading as Best Pension Annuity operate an ‘utmost good faith’ policy. This means that both Platinum and the customer are working openly and honestly with each other with the genuine aim of concluding this business to their mutual benefit.

All flexible drawdown transactions are on a non-advised basis. This means that it is the customers responsibility to ensure that the product is suitable for their needs. The decision to use flexible drawdown is entirely at the customers own discretion.

We offer one product from one provider for flexible drawdown. We chose a provider that offers the flexible drawdown features discussed on this website.

We will provide all customers with a personalised quote, key features document and information pack BEFORE the customer submits an application.

Genuine circumstances may occur that cause the business not to complete. Platinum has an obligation to treat customers fairly and equally in ‘utmost good faith’. For this reason we have introduced a no fee condition to cover situations where the business does not complete. |

| |

|

|

|

|

|

ABOUT US | INITIAL DISCLOSURE | FREE ANNUITY GUIDE | TERMS & CONDITIONS | PRIVACY POLICY | CONTACT US | SITEMAP | NEWS | BLOG

Cookies Policy : The website does not use cookies and nothing is downloaded to your PC or Device

The information contained on this website is for information purposes only.

This website DOES NOT contain personal advice based on your circumstances.

Platinum Financial Consulting

Platinum Financial Consulting LTD

Registered in England. Company Number : 5985049

Registered Office Address :

The Old School House, East End Road

Bradwell-on-Sea, Essex, CM0 7PY

Telephone : 020 33 55 4827 Fax : 0871 277 1422 Email : info@platinumifa.co.uk

FCA Registration Number : 827778

|

|

If you are nearing retirement keep up to date with annuity rate changes by subscribing to our news feed |

Pension Annuity Specialists

|

|

|